Midland Paper reports a reduction of over 3 billion tons – 6.148 trillion pounds – of paper production through Q3 due to multiple mill / machine closures. The first six months of the year resulted in 10 mill price increases and two ink price increases; additional increases are expected throughout the remainder of the year. The price of fuel and truck driver shortages continues to challenge the transportation industry directly impacting paper costs. Highway diesel fuel has increased more than 30% over the past year.

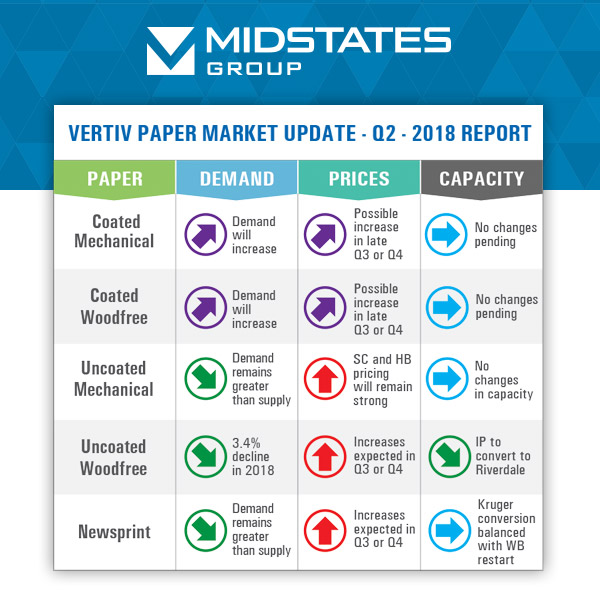

Coated Mechanical

No changes in CGW capacity. Mills are expected to raise prices again in September. Coated mechanical continues to be tight. Mills are reported sold out or are overbooked through Nov/Dec. Customers are highly encouraged to order paper now due to limited supplies available for the robust fall and winter seasons.

Coated Woodfree

No changes in CFS capacity. Two CFS mills announced price increases for September. Other CFS mills are expected to follow suit. Coated Freesheet continues to be tight going into the second half of the year. Customers are highly encouraged to order paper now due to limited supplies available for the robust fall and winter seasons.

Uncoated Mechanical

Shipments to capacity is just over 100% through June 1st although a 6.4% decrease is expected in the second half of 2018. The ITC will vote on August 28th to determine if the tariffs are warranted. High-Brite and SC inventories remains very tight. The majority of mills are sold out for the remainder of the year and are looking for relief. The market demand is expected to outpace supply until the end of 2018. SC prices are expected to increase in Q3.

Uncoated Woodfree

Demand was down -1.7% through June 1st while shipments were up 3% resulting in 92% shipping capacity. Expect further price increases in 2018. Mills are sold out of white offset therefore customers are upgrading to Opaque which is causing the Opaque market to quickly reach sold-out status.

Newsprint

Demand is down -9.2% while shipments to capacity are at 95%. Major suppliers have either declined to ship to the US in August or are drastically cutting their shipment volumes. Newsprint is currently sold out and is expected to remain sold out throughout 2018.